Summary:

Global commodity markets witnessed heightened volatility during H1 2026, driven by geopolitical tensions, a stronger US dollar, and shifting demand-supply dynamics. Precious metals touched record highs before correcting sharply, while base metals delivered mixed returns led by zinc and aluminium. Energy markets remained volatile, with crude oil rallying on Middle East tensions before easing, making H1 2026 a dynamic period across commodities.

The first half of 2026 is now behind us, and it proved to be an exceptionally volatile and eventful period for global commodity and currency markets. A strengthening US Dollar, a resilient US economy, and rising geopolitical tensions dominated market sentiment throughout the period. These factors propelled several commodities to both lifetime highs and steep corrections in same period.

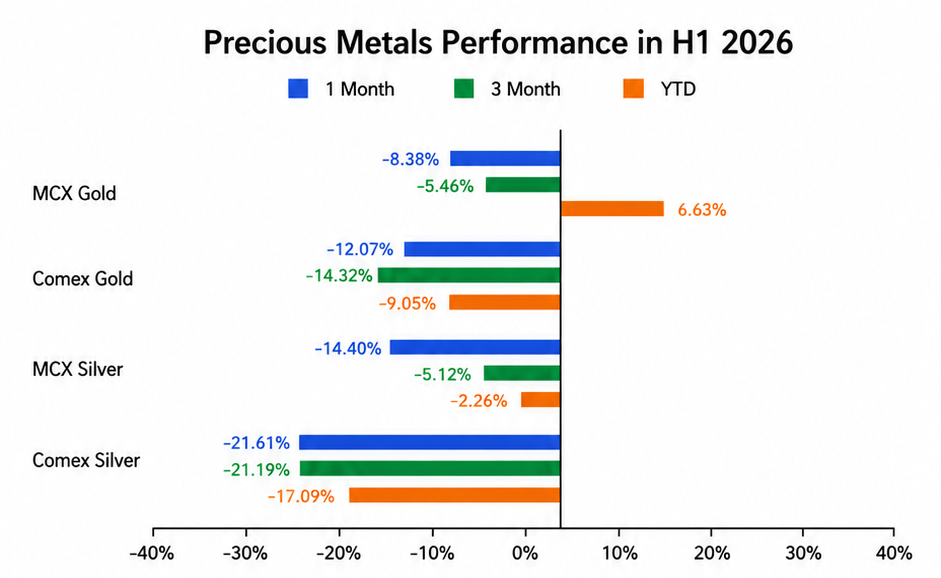

Precious Metals Performance in H1 2026:

Gold and Silver started 2026 on a strong note, particularly in January, driven increasing speculative and ETF demand and physical shortage, with both metals surging to decade highs. Gold touching an all-time high of nearly 5598 on COMEX and 180779 on MCX, while Silver climbed to 121.63 on COMEX and 420048 on MCX. Following these record highs, both metals witnessed sharp technical selling and profit booking, with bearish momentum accelerating further as the US Dollar strengthened. Despite the steep correction, MCX Gold delivered a 6.63% YTD return during the first half of 2026, while on COMEX Gold declined 9.05% over the same period. Silver underperformed Gold, with MCX Silver slipping 2.26% YTD, whereas COMEX Silver fell 17.09%. The divergence between domestic and international prices was largely driven by the weakening Indian Rupee and import duty hikes, which helped cushion losses in MCX contracts.

Explore: Why silver may outperform gold in 2026

Base Metals Performance in H1 2026:

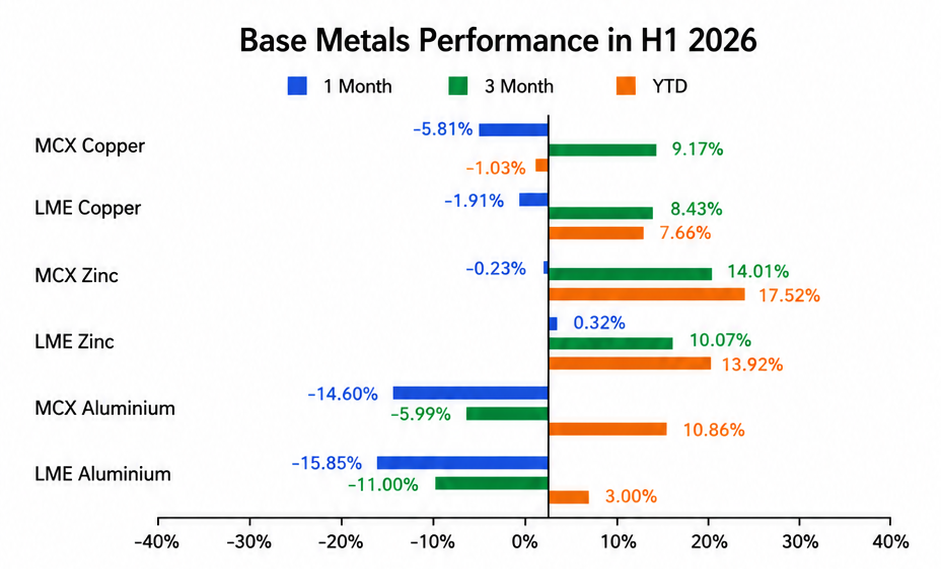

Base metals delivered mixed performance during the first half of 2026, influenced by supply disruptions, inventory trends, and geopolitical developments. Zinc emerged as the top performer, with MCX Zinc gaining 17.52% YTD and LME Zinc rising 13.92%, supported by tight mine supply and improving demand expectations. Copper touched a lifetime high of 1480.30 on MCX in January before correcting sharply and later recovering part of its losses; on a year-to-date basis, MCX Copper declined 1.03%, while LME Copper gained 7.66%, indicating relatively stronger international performance. Aluminium also reached a lifetime high of nearly 397 during the Iran–US conflict amid supply concerns, and despite a recent correction, remained positive for the period, with MCX Aluminium gaining 10.86% and LME Aluminium advancing 3.00%.

Explore: Introduction to Commodity Trading

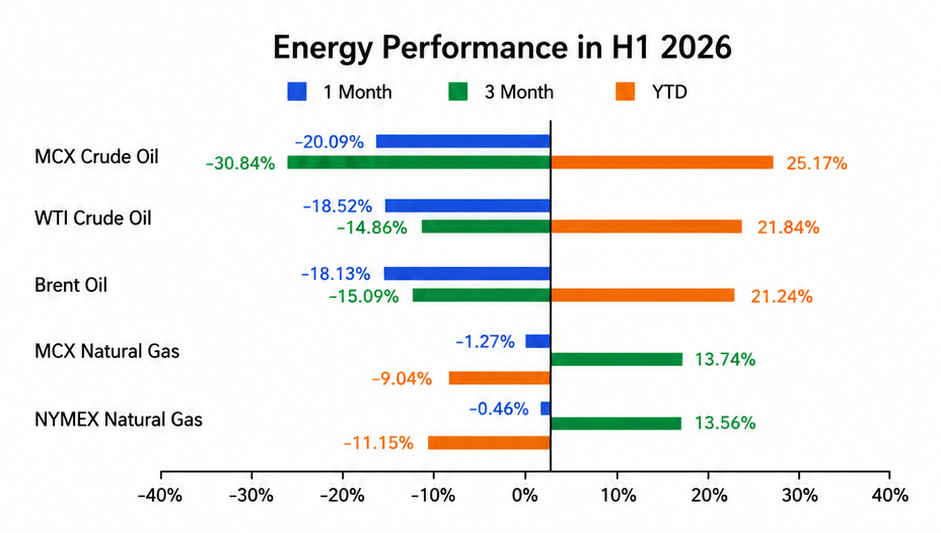

Energy Performance in H1 2026:

Energy commodities, particularly Crude Oil and Natural Gas, remained in sharp focus during the first half of 2026 amid heightened geopolitical tensions and shifting demand-supply dynamics. Crude oil traded largely range-bound during the first quarter due to expectations of rising global supplies and concerns over slowing demand. However, prices surged as Middle East tensions escalated and fears of supply disruptions through the Strait of Hormuz intensified, pushing MCX Crude Oil to an all-time high of 10990 and WTI Crude Oil to 119.47 per barrel. Prices later corrected sharply as geopolitical tensions eased. Despite this volatility, MCX Crude Oil gained 25.17% during H1 2026, while WTI Crude Oil advanced 21.84%. Meanwhile, Natural Gas started the year on a strong note, supported by robust winter heating demand, before retreating and trading in a relatively stable range for the remainder of the half. Overall, MCX Natural Gas declined 9.04% during H1 2026, while NYMEX Natural Gas fell 11.15%, reflecting easing weather-driven demand and improved supply conditions.