Summary:

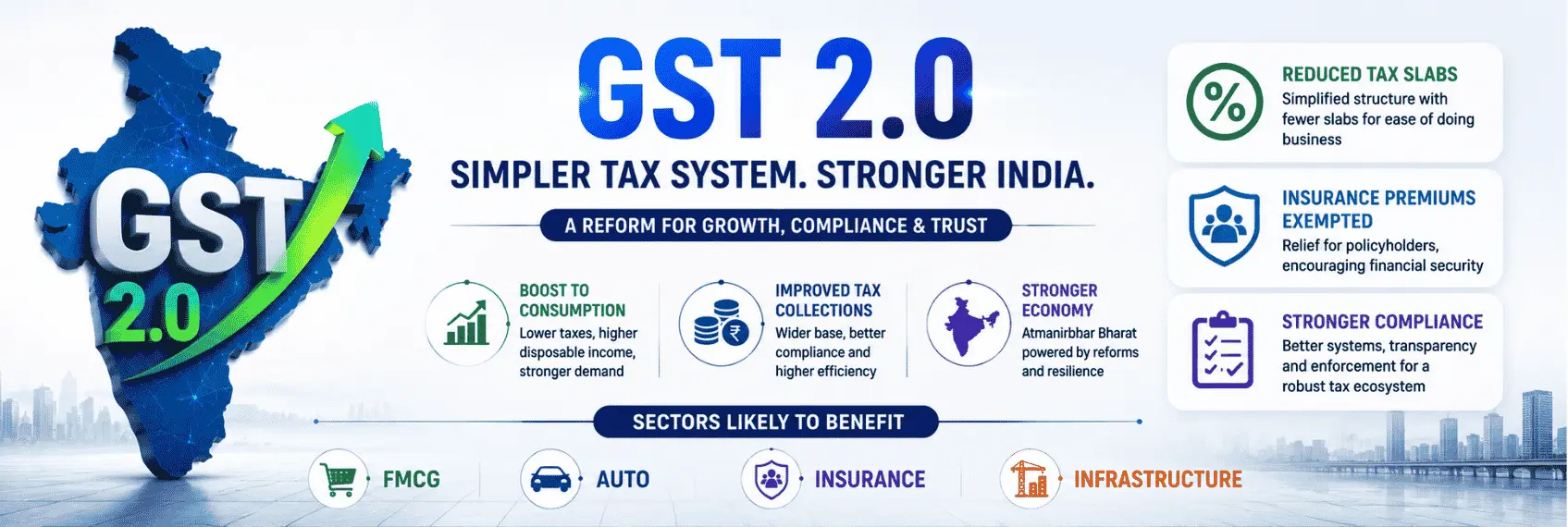

GST 2.0 simplifies India's indirect tax structure by reducing tax slabs, exempting insurance premiums, and strengthening compliance. The reform is expected to boost consumption, improve tax collections, and influence sectors such as FMCG, auto, insurance, and infrastructure.

Ask any shopkeeper in Pune's Laxmi Road or any CFO in a BKC boardroom, and they'll tell you the same thing, GST 2.0 has changed how India does business. Rolled out from September 22, 2025, on the eve of Navratri, this is the most sweeping rework of our indirect tax system since GST itself was born in July 2017. For an investor, it's not just a tax story. It's an earnings story, a consumption story, and honestly, a compliance headache too if your systems aren't updated.

The New GST Tax Slabs List: From Five Slabs to Two (Plus One)

The old structure of 0%, 5%, 12%, 18% and 28% is gone for most goods. GST 2.0 has compressed this into essentially two working slabs, 5% and 18%, with a steep 40% rate reserved for sin and luxury goods like tobacco, pan masala, aerated drinks, and high-end cars. Gold and jewellery still sit outside this at 3%, and rough diamonds at 0.25%, untouched by the reform.

What does this mean in rupee terms? A ₹50,000 refrigerator that earlier attracted 28% GST now costs roughly ₹5,000 less in tax alone. Household staples, soap, shampoo, toothpaste, hair oil, moved from 18% down to 5%. Ghee, butter, and paneer slid from 12% to 5%. Health and life insurance premiums are now GST-exempt, a genuine relief for retail policyholders. On the flip side, coal jumped from 5% to 18%, which quietly raises input costs for power, cement, and steel companies, something I'd watch closely if you're holding names in those sectors.

GST Collections: The Numbers Tell Their Own Story

For June 2026, gross GST collections came in at ₹1,94,812 crore, up 13.9% year-on-year from ₹1,71,105 crore in June 2025. Net collections, after refunds, stood at ₹1,62,377 crore, an 11.2% rise. Interestingly, the growth wasn't purely domestic, import-linked IGST surged 34.6% to ₹60,038 crore, while domestic revenue grew a more modest 6.5%. For the April–June quarter of FY27, cumulative gross collections touched ₹6,31,699 crore, up 8.4% over last year. Maharashtra, unsurprisingly, remained the top contributor among states at ₹30,714 crore for the month, a 9% jump. These aren't just bureaucratic figures, sustained collections above ₹1.9 lakh crore a month tell you formal consumption and compliance are both holding up, which is a genuinely healthy signal for GDP-linked equity themes. GST Calculator

Compliance Side: What's Changed for Businesses and MSMEs

If you run a business or track one, the compliance calendar hasn't moved, GSTR-1 is still due on the 11th of the following month, and GSTR-3B by the 20th (22nd or 24th for QRMP filers, depending on state). But enforcement has sharpened. E-invoicing is now mandatory for turnover above ₹5 crore, and there's active discussion of pulling that threshold down to ₹2 crore by FY27, which would sweep in a lot more MSMEs. AI-based scrutiny now automatically flags GSTR-1 versus GSTR-3B mismatches, so late fees and even GST cancellation risk are less forgiving than before. The e-way bill system continues to require generation for movement of goods above ₹50,000, with validity typically one day per 200 km. For anyone verifying a vendor or a listed company's subsidiary, a quick GST number search or GSTIN check on the GST portal remains the fastest sanity check on genuineness before you extend credit or sign a contract.

The composition scheme, GST registration limits (₹40 lakh for goods, ₹20 lakh for services in most states), and HSN-code-based rate mapping remain the backbone of day-to-day compliance, but with 12% and 28% gone, a lot of HSN-to-rate mappings needed re-verification, and I've seen more than a few businesses caught off guard invoicing at the wrong rate in October and November last year.

The Investor Takeaway

GST 2.0 is a demand-side lever dressed up as a tax reform. FMCG, consumer durables, and insurance are the clearest beneficiaries; cheaper end-products historically translate into volume growth, which shows up in quarterly numbers with a lag of two to three quarters. Auto, especially small cars and sub-350cc two-wheelers now at 18% instead of 28%, is worth tracking for a replacement-cycle bump. Coal, cement, and power names carry a fresh cost overhang worth pricing in. As always, don't chase the headline; read the management commentary in the next two earnings calls before you decide whether the tailwind is priced in or not.