Prefer direct plans to regular plans: This is a standard piece of advice you often get nowadays when it comes to mutual fund investing. We believe that instead of making it a direct vs regular mutual fund contest, investors would be better off deciding for themselves what works best for them.

Which is better, direct or regular mutual fund?

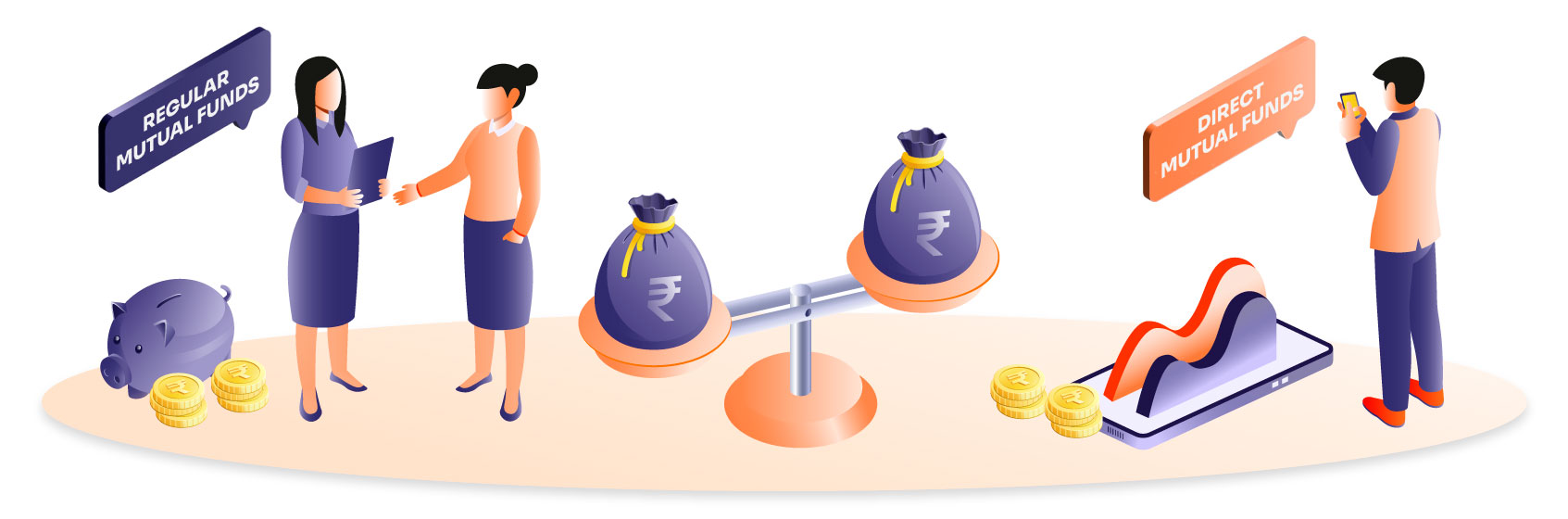

Did you know this fact about a regular vs direct mutual fund?

The underlying portfolio of a direct and regular mutual fund is identical. Meaning, you will have exposure to precisely the same assets/securities whether you invest in a direct or regular mutual fund.

What differentiates a direct mutual fund from a regular mutual fund?

Every mutual fund scheme charges its investors a fee, collected as an expense ratio. A direct plan and a regular plan are two options investors get while investing in mutual funds. Direct plans typically have lower expense ratios and regular plans have relatively higher expense ratios.

The primary difference between direct and regular mutual funds is distribution expenses. Under regular plans, mutual fund houses pay commissions to their distribution and channel partners while direct plans save these costs and pass on the benefits to investors in the form of a lower expense ratio.

The concept of direct plans isn’t new, and in fact, direct plans have existed since January 2013. But they took off only over the last 4-5 years.

Why are direct mutual funds becoming popular?

Convenience in investing has improved substantially with the advent of new-age fintech platforms. Mutual fund houses have also been investing heavily in technology to improve the user experience. As a result, investing in mutual funds using an app has become as simple as transferring money online. And many experts and investors believe that there’s no real need to route your investments through a distributor/broker. Well, this might be true for those who are well-versed in equity and debt markets, but definitely not for all.

Proponents of direct plans draw attention to the fact that 0.5%-1% of savings in expense ratios through direct plans would enhance your wealth considerably. Many investors interpret this incorrectly. The potential savings on account of choosing direct plans come only when you invest in very competitive funds that are likely to outperform the competition and their respective benchmarks.

Want to choose between a direct vs regular mutual fund? Ask yourself three questions:

- Are you a well-read investor who knows the market in and out?

- How confident are you pertaining to the choice and suitability of a mutual fund scheme?

- Would you prefer an expert who can guide you better?

If your answer to any two of the above questions was in the affirmative, you might want to go with regular plans.

Please don’t forget that responsible mutual fund distributors not only help mutual fund investors understand product suitability and nuances, but they also behave like your true friends when markets are rocky. Those who have experienced harsh bear markets in the past would know how vital conversations with your mutual fund distributors are under falling markets.

In brief, which is better direct or regular mutual fund?

We firmly believe that there’s no one answer to this question. It depends on how much time you can dedicate to managing your mutual fund investments and what your investment quotient is. If you are a savvy investor and can pick the right mutual funds without any professional help and perfectly manage your portfolio on your own, direct plans may work best for you. However, many people still prefer regular plans regardless of their knowledge because there are experts who can guide them in the process and through any market challenges.

After all, comparing costs is important, but not at the expense of scheme performance. Choose your options wisely.

Happy investing!

Post your comment

You must be logged in to post a comment.