Summary:

Two of the most widely used directional options strategies look similar on paper but serve very different market outlooks. Here's how to tell them apart, and more importantly, when each one actually earns its place in your portfolio.

Options traders love vertical spreads for one simple reason: they let you take a directional view on a stock while keeping risk firmly defined. But the choice between a bull call spread and a bear put spread trips up a lot of people, not because the mechanics are complicated, but because the conditions that make each strategy genuinely useful are often misunderstood.

Let's fix that. Rather than just explaining the textbook definitions, this piece gets into the real-world logic of each trade, when to reach for one over the other, what the payoff pictures actually mean, and how to avoid the common mistakes that eat into returns.

The Bull Call Spread: Betting on a Move Up, at a Discount

A bull call spread is constructed by buying a call option at a lower strike price and simultaneously selling a call at a higher strike price, both on the same underlying and with the same expiration. The premium you collect from selling the higher-strike call offsets part of the cost of the option you bought. That's the whole point — you pay less upfront, which lowers your break-even and improves your risk-reward ratio, at the cost of capping your maximum profit.

Think of it this way: you're saying "I think this stock is going up, but I'm not convinced it's going to the moon." You're happy to give up the tail-end gains in exchange for a cheaper entry.

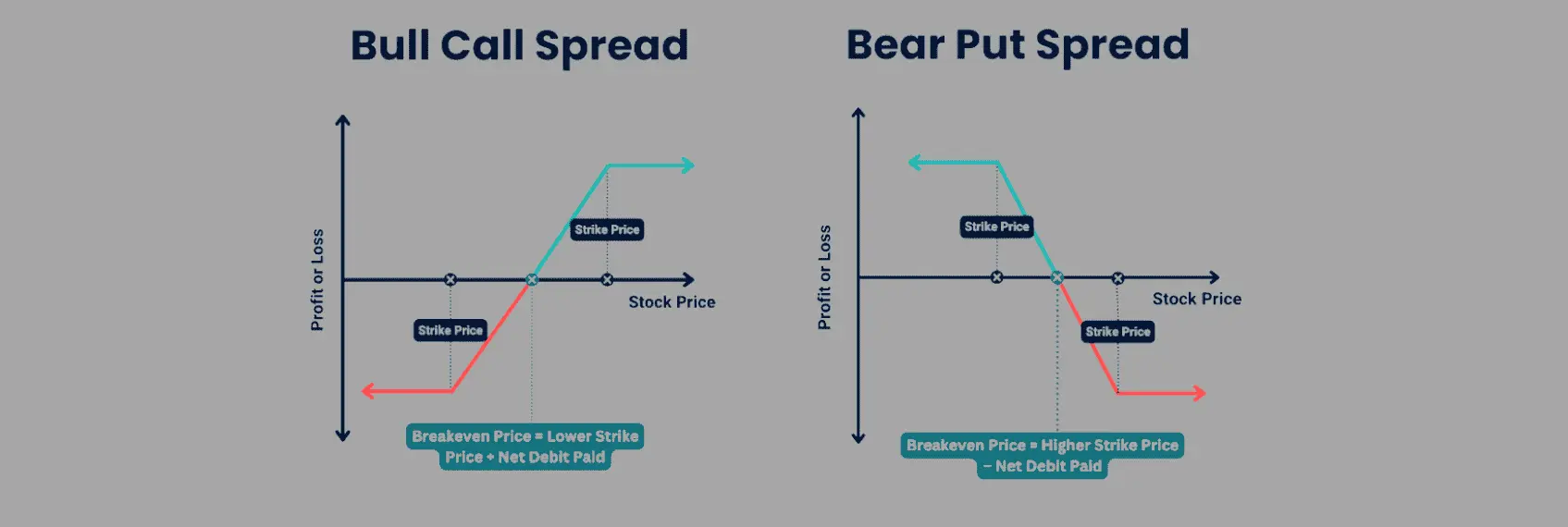

Bull Call Spread

Buy lower-strike call, sell higher-strike call. Net debit trade. Profits when underlying rises above break-even. Max gain is capped at upper strike.

Bear Put Spread

Buy higher-strike put, sell lower-strike put. Net debit trade. Profits when underlying falls below break-even. Max gain is capped at lower strike.

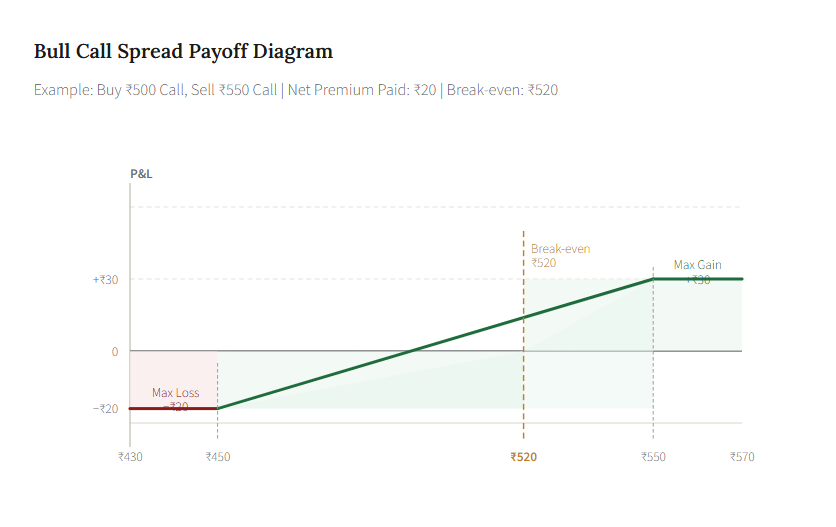

Bull Call Spread - Payoff at Expiration

The payoff chart tells the whole story at a glance. Below the lower strike (where you bought the call), you lose the entire premium paid — that's your maximum loss, and it's fixed. Above the upper strike (where you sold), your profit maxes out. Everything in between is a linear slide from loss to gain, with the break-even sitting somewhere between the two strikes depending on what you paid.

The Bear Put Spread: Profiting From a Decline, Without the Full Cost

The bear put spread is the mirror image. You buy a put at a higher strike and sell a put at a lower strike. The sold put brings in premium that offsets the cost of the put you bought, but it also caps how much you can make if the stock falls hard. You're expressing a bearish view — just not an apocalyptic one.

This is particularly useful when you think a stock is due for a pullback but not a complete collapse. Buying a naked put in that scenario would cost more and require a larger move to become profitable. The spread keeps things tidy.

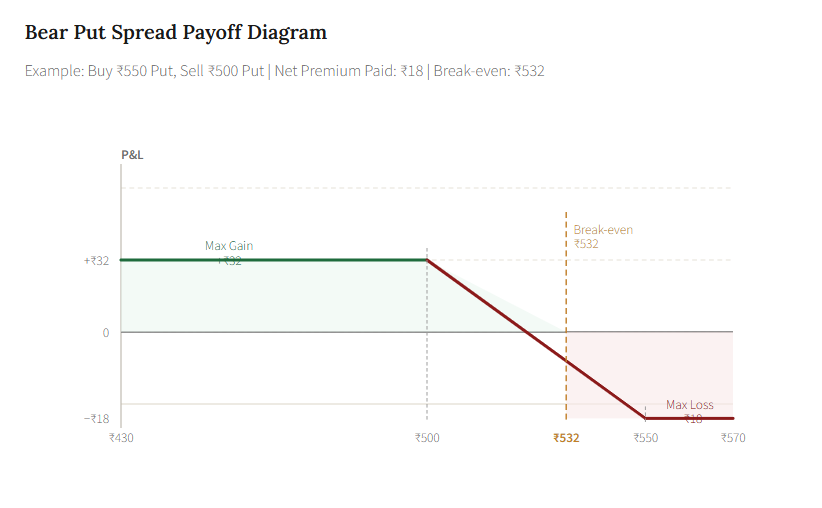

Bear Put Spread - Payoff at Expiration

Side-by-Side: The Numbers That Matter

| Factor | Bull Call Spread | Bear Put Spread |

| Market View | Moderately bullish | Moderately bearish |

| Construction | Buy lower strike call + Sell higher strike call | Buy higher strike put + Sell lower strike put |

| Net Cash Flow | Net debit (you pay) | Net debit (you pay) |

| Max Loss | Premium paid | Premium paid |

| Max Gain | Spread width − premium paid | Spread width − premium paid |

| Break-even | Lower strike + premium paid | Higher strike − premium paid |

| Profits When | Underlying price rises | Underlying price falls |

| Time Decay Effect | Hurts when OTM, helps when ITM | Hurts when OTM, helps when ITM |

| Best Used With | Low to moderate IV environment | Elevated IV (relatively cheaper puts) |

The Context That Changes Everything

Consider implied volatility. When IV is running high, say, ahead of an earnings report or during a market-wide spike in the VIX, both calls and puts are expensive. A bear put spread in this environment still costs you real money, but the higher IV means the absolute premium on the put you're selling is also elevated, which gives you a better offset. For a bull call spread, high IV works against you somewhat since you're buying more premium than you're selling in net cost terms.

A useful rule of thumb: In high-IV environments, spreads make more intuitive sense than naked long options because the net debit you pay is relatively lower compared to the potential gain. The premium compression from the short leg becomes more meaningful when IV is inflated.

When to Use Each - Practical Scenarios

Scenario A — Use a Bull Call Spread

Stock has pulled back to a well-tested support level

Nifty has fallen to a support zone where it has bounced multiple times. You're not expecting a massive rally — just a moderate recovery of 3–5%. A bull call spread lets you capture this move cheaply, with the sold call acting as a ceiling you're comfortable with.

Scenario B — Use a Bear Put Spread

Sector rotation is underway and the stock is hitting resistance

A mid-cap IT stock has had a strong run and is now stalling near a multi-month high. Valuations look stretched. You expect a 4–6% correction, not a collapse. A bear put spread hedges the downside cleanly without blowing out premium on a naked put.

Scenario C — Avoid Both

High conviction, massive expected move

You have strong conviction that a stock will move 20%+ in one direction — perhaps ahead of a binary event. In this case, the capped profit from a spread may leave a lot on the table. A naked long option or another structure might serve you better if your conviction is that high.

The Quick Decision Framework

Which spread fits your current view?

| Factor | Guidance |

| Market View | Bullish → Bull Call Spread | Bearish → Bear Put Spread |

| Move Size | Moderate move (3–8%) favors spreads; large move favors naked options |

| Implied Volatility (IV) | Low-to-moderate IV preferred; high IV increases net debit cost |

| Time Horizon | Short-term for high conviction; longer expiries for flexibility |

| Risk Budget | Max loss limited to net premium paid (defined risk strategy) |

A Final Word on Execution

Both spreads are what traders call "defined risk" trades, you know your worst case before you enter. That's genuinely valuable in volatile markets. But defined risk doesn't mean riskless. Many traders lose consistently with these strategies not because the structures are flawed, but because they enter without a clear thesis on why the move is likely, how big it's likely to be, and over what time frame.

The spread you choose matters far less than whether your directional view is rooted in something real, a technical level, a fundamental catalyst, a macro shift. Without that foundation, even the most elegantly structured options trade becomes an expensive guess.

Used thoughtfully, though, these two strategies give you some of the cleanest risk-reward profiles available in the options market. And once you're comfortable with the mechanics, they become a natural part of how you think about taking directional positions.