Summary:

If you own shares and wish they'd work a little harder, the covered call is one of the oldest tricks in the book, and one of the most consistently useful. Here's the full picture, from mechanics to execution.

Owning stocks is one thing. Getting them to generate income on top of any dividends or price appreciation is another entirely. That's where the covered call enters the picture, a strategy that turns your existing holdings into something closer to a yield-generating asset, month after month, without requiring you to sell a single share (most of the time).

It's not a magic trick, and there are real trade-offs worth understanding. But for long-term investors sitting on positions they intend to hold anyway, covered calls are one of the most capital-efficient tools in the options toolkit.

How It Actually Works

At its core, a covered call means selling a call option on a stock you already own, for a strike price above the current market price. In exchange, the buyer pays you a premium upfront. That premium is yours to keep, regardless of what the stock does.

The "covered" part matters. It means you already own the underlying shares. If the buyer exercises the option (because the stock rose above the strike), you deliver shares you already have. You're not exposed to the potentially unlimited loss of a naked call. Your worst case isn't unlimited downside — it's simply that you sell your shares at the strike price, which may be below the current market price if the stock has shot up sharply.

- You own 100 shares of the stock — these act as your “cover”

- You sell 1 call option with a strike price above the current market price

- You receive premium upfront, which is yours to keep regardless of what happens next

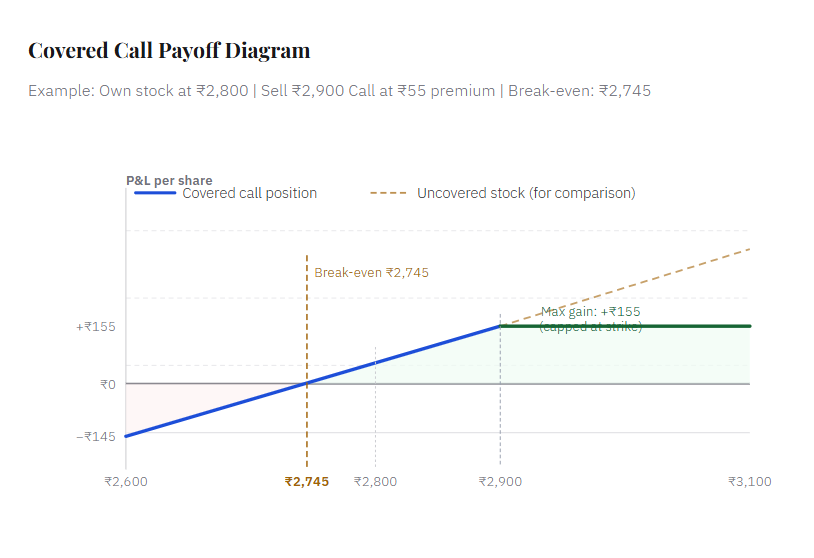

A Worked Example

| Factor | Details |

| Stock | Reliance Industries |

| Current Stock Price | ₹2,800 per share |

| Shares Owned | 100 shares (₹2,80,000 total) |

| Call Strike Selected | ₹2,900 (3.6% above market price) |

| Expiry | Monthly (28 days out) |

| Premium Collected | ₹55 per share = ₹5,500 total |

| Annualised Yield (Approx.) | ~23.6% on the position |

That ₹5,500 sits in your account immediately. It cushions any downside and adds to your return if the stock stays put or moves up moderately. The trade-off: if Reliance rallies to ₹3,100, your upside is capped at ₹2,900, you'd miss out on the ₹200 gain above your strike.

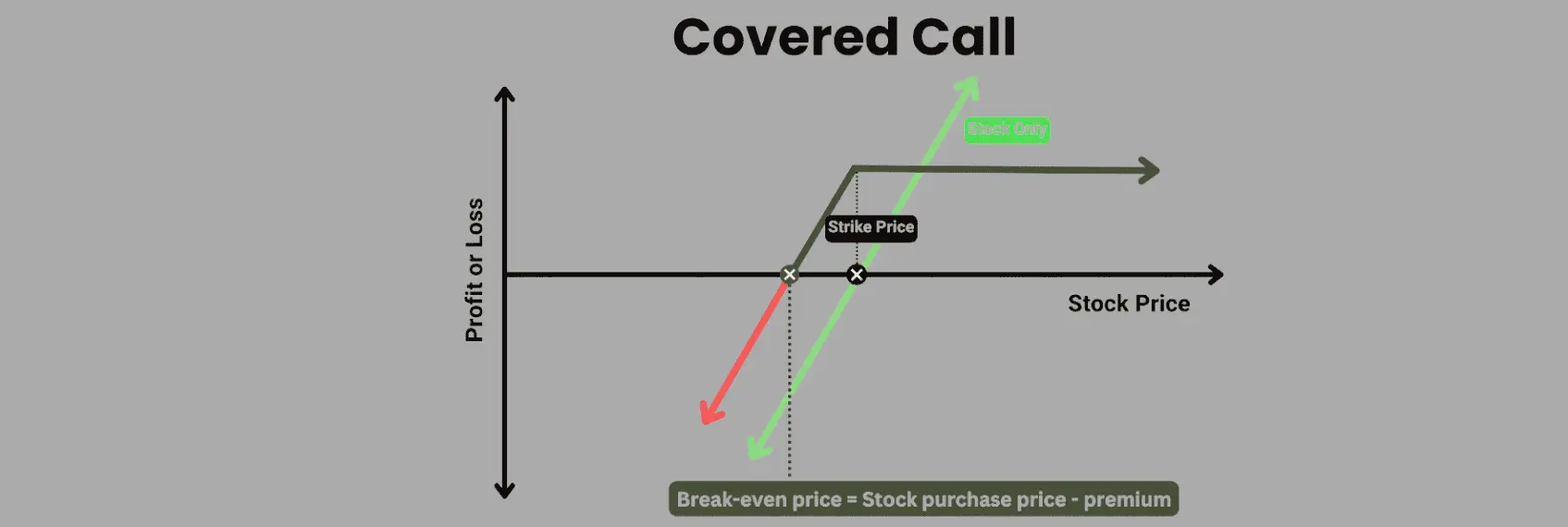

The Payoff Picture

Covered Call - Payoff at Expiration

The blue line is your covered call position. Notice how it rises in line with the stock up to the ₹2,900 strike, then goes flat; that's where the sold call kicks in and caps your gains. The dotted gold line shows what you'd have earned if you'd simply held the stock outright, without selling the call. Above the strike, you miss out on that additional appreciation. But below the strike, and especially in flat or mildly declining markets, the covered call is clearly superior because of the ₹55 premium you collected.

The Three Scenarios - And What You Keep

Stock stays flat

If the stock price doesn’t move much, the option expires worthless. You keep the full ₹55 premium and continue holding all your shares. This is the ideal scenario, as you earn income without losing your position.

Stock rises above the strike price

If the stock moves above ₹2,900, the option is likely to be exercised. Your shares will be sold at ₹2,900. You earn a ₹100 capital gain (₹2,900 − ₹2,800) plus the ₹55 premium. While you make a profit, your upside is capped and you miss any gains beyond ₹2,900.

Stock falls

If the stock declines to ₹2,700, the option expires worthless. You still keep the ₹55 premium, which helps offset the loss. Instead of a ₹100 loss, your net loss is reduced to ₹45. The premium provides partial protection, but it does not eliminate downside risk.

The core insight: A covered call doesn't eliminate the risk of owning a stock. If the stock falls 30%, the ₹55 premium is a consolation, not a solution. The strategy works best on positions you intended to hold regardless, it's an income layer, not a hedge.

Choosing the Right Strike Price

Strike selection is where the real craft of covered call writing lives. Go too far out-of-the-money and the premium is negligible. Go too close to the current price and you risk having your shares called away at a price you're not comfortable with, or you choke off the stock's room to appreciate.

Strike Selection Guide

Aggressive (OTM 1–3%)

Higher premium but close to current price. Greater chance of assignment. Good for flat-market income, not ideal if you want price participation.

Balanced (OTM 3–6%)

The sweet spot for most long-term holders. Decent premium, reasonable buffer before assignment, allows modest upside in the stock.

Conservative (OTM 6–10%)

Lower premium, but you're giving the stock more room to run. Better when you're uncertain about the timing but still want some income.

Deep OTM (10%+)

Very small premium. Mostly meaningful during very high IV periods when far-out premiums are still worthwhile. Often not worth the complexity otherwise.

When to Use the Covered Call

| Situation | What to Do |

| Neutral to mildly bullish view | Ideal setup. You don't expect a big move; collecting premium is the point. Roll the trade each month. |

| Approaching a sell target | Sell a call at your target price. If it's hit, you get called out at a price you were happy to sell anyway — plus you kept the premium. |

| IV is elevated | Higher implied volatility means richer premiums. A spike in VIX or stock-specific IV is a good time to write covered calls. |

| Strongly bullish view | Think carefully. Selling a call limits your upside. If you're very bullish, just hold the stock and collect no premium. |

| Bearish view on the stock | Wrong tool. The premium won't protect you from a serious drawdown. Consider reducing position size instead. |

Managing the Trade After Entry

Not every covered call expires cleanly on expiry day. Knowing how to manage mid-trade surprises separates consistent practitioners from casual experimenters.

If the stock rises sharply toward your strike well before expiration, you have a choice: let it be, and risk assignment, or "roll up and out" — buying back the short call and selling a new one at a higher strike with a later expiry. Rolling gives you more upside room but costs you some of the original premium.

If the stock falls and the option is deep out-of-the-money with little time value remaining, you can buy back the call cheaply and sell a new one at a lower strike to collect more premium. This is called "rolling down." It increases the premium income but also lowers the break-even further.

Advantages

- Generates regular income from existing holdings

- Reduces effective cost basis over time

- Limited additional capital required

- Risk is defined — you already own the shares

- Profitable in flat and mildly rising markets

- Can be layered with dividend income

Limitations

- Caps upside — you miss big rallies above the strike

- Doesn't protect against serious downturns

- Tax implications on the premium received

- An assignment can be inconvenient if unexpected

- Requires 100 shares per contract (capital intensive)

- Repeated rolling can become time-consuming

The Long Game: Compounding Premium Over Time

One of the underappreciated aspects of covered call writing is what happens when you treat it as a long-term discipline rather than a one-off trade. If you're collecting 1.5–2% per month in premium on a blue-chip position you plan to hold for years, that adds up to meaningful yield enhancement, potentially 15–20% annualised on top of dividends and any capital appreciation up to your strike.

The catch, as always, is that you'll have months where the stock makes a significant move above your strike, and you'll feel you left money on the table. But over many cycles, the premium income tends to more than compensate for those missed gains, particularly in choppy or range-bound markets where uncovered holders are simply waiting.

The covered call rewards patience and consistency more than brilliance. You don't need perfect market timing. You need a stock you're comfortable owning, a strike you'd be happy selling at, and the discipline to repeat the process month after month, in up markets and sideways ones alike.

For investors looking to extract more from their portfolios without taking on additional risk capital, that's a genuinely compelling proposition.