Summary:

Gold prices corrected sharply after record highs amid geopolitical tensions and rising volatility. Despite near-term pressure from strong dollar and yields, central bank demand, ETF growth, and global uncertainty support a positive long-term outlook.

Gold prices witnessed a sharp correction during February and March after an extended rally that pushed prices to record highs. The decline gathered further momentum following the onset of the Iran conflict, with prices retracing a significant portion of the earlier gains amid increased volatility. On the MCX, gold briefly breached the ₹130,000 mark, correcting from January highs near ₹180,000, before finding support and staging a modest recovery.

Macroeconomic Context:

Geopolitical risk is currently the primary driver of market price action, with the US–Iran conflict and the blockade of the Strait of Hormuz disrupting global trade and sentiment. Despite gold’s safe-haven status, prices saw notable liquidation in the initial phase as capital moved towards the US dollar and Treasuries amid heightened uncertainty.

Rising energy prices have pushed inflation expectations higher, forcing central banks into a cautious stance. Markets are now pricing in a slower pace of monetary easing, with expectations of rate cuts by the Federal Reserve being pushed further out, keeping financial conditions tight and capping near-term upside in gold.

Another important dynamic is the typical market behaviour during the early stages of major conflicts. Gold often corrects initially, as broad-based risk-off moves across asset classes trigger margin calls and forced liquidation. This effect has been more pronounced given the strong rally gold experienced through last year up to January, making it vulnerable to profit booking.

However, as the conflict prolongs, the risk premium in gold is likely to build gradually. Continued uncertainty and potential spillover effects are expected to provide underlying support to prices over time. In addition, the ongoing Russia–Ukraine conflict continues to heighten geopolitical risk, reinforcing gold’s role as a strategic hedge in the current environment.

Central Bank & Institutional Demand:

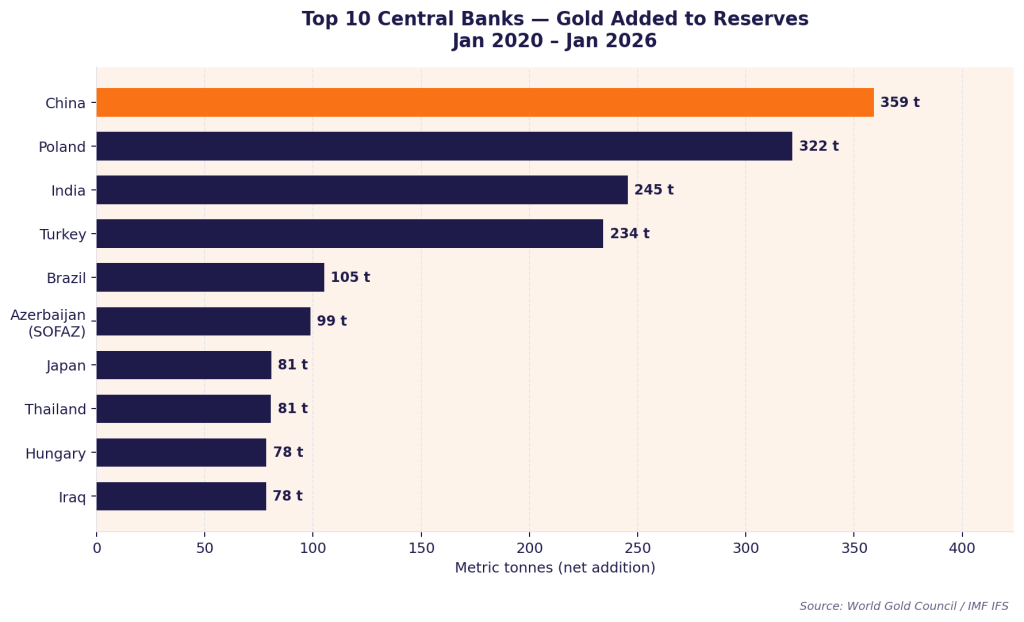

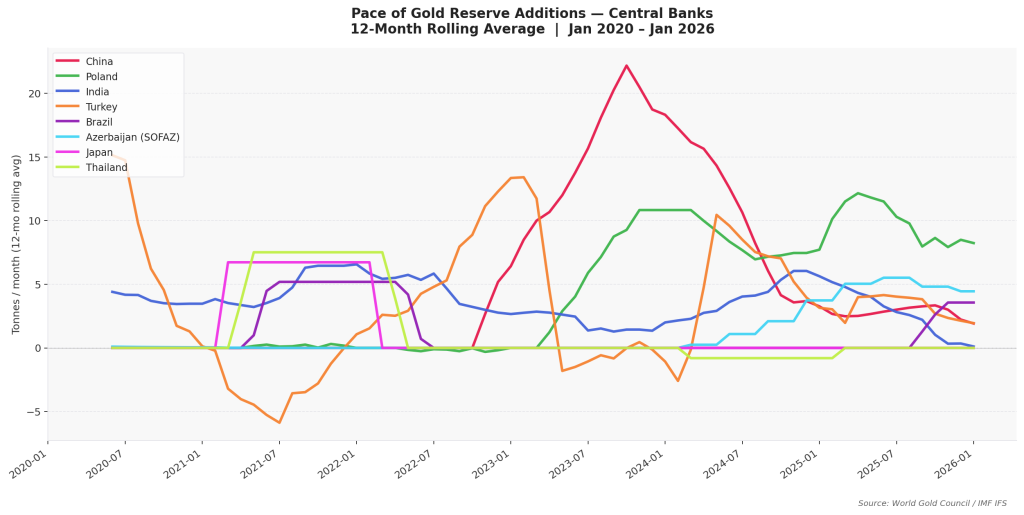

Over the past 3–4 years, central bank purchases have emerged as a key structural pillar supporting gold demand. Since January 2020, China has been the largest buyer, adding approximately 359 tonnes to its reserves, followed by Poland with 322 tonnes and India with 245 tonnes, according to the World Gold Council. This trend gained further momentum after the Ukraine–Russia war, as governments looked to diversify their reserves.

While central banks remain net buyers, the pace of accumulation has moderated. Recent developments suggest that gold is also being used as a source of liquidity, with some central banks facing pressure on dollar availability due to elevated energy prices and external imbalances. For instance, Turkey has engaged in gold swaps to raise dollar liquidity, while Russia has reportedly sold a portion of its reserves.

Despite this, central bank demand continues to act as a structural floor for gold prices. Even with moderation, baseline demand remains significantly higher than pre-2022 levels.

ETF Demand:

| Annual %Change in Holdings: Key Global Gold ETFs | ||||

| Region | Name of fund | 2024 | 2025 | YTD |

| US | SPDR Gold Shares | 2.51% | 23.80% | 1.31% |

| India | Nippon India ETF Gold BeES | 42.10% | 45.84% | 2.42% |

| China | Huaan Yifu Gold ETF | 62.36% | 109.38% | -1.12% |

| Source: World Gold Council | ||||

INR & Domestic Factors:

USDINR has remained volatile, briefly breaching the 95 level before recovering on the back of central bank intervention to curb speculative pressures. Despite this correction, the rupee has weakened by over 4% in just the first three months of the year, highlighting underlying fragility. Broader fundamentals continue to point towards sustained weakness, with a widening trade deficit and persistent FII outflows weighing on the currency. This is further reflected in the rise in dollar-rupee forward premiums. The weakness in the domestic currency has acted as a key support for gold prices, cushioning downside in MCX gold and leading to relative outperformance compared to international benchmarks.

Why Gold Remains Positive in the Medium to Long Term

Chaos Premium:

The global economy is navigating an era of unprecedented volatility, where the weaponization of trade and escalating kinetic warfare have placed existing supply chains under systemic strain. The protracted Russia-Ukraine conflict remains a persistent drain on European energy security, while the Middle East crisis has transitioned from a localized friction into a broader regional confrontation involving Iran, Israel, and the United States.

In this landscape, gold’s role as a "crisis hedge" is being revitalized. The spike in energy costs—with Brent Crude testing the $100–$120 range, has reignited global inflationary pressures while simultaneously dampening industrial output. This creates a high-probability Stagflationary scenario: a toxic mix of slowing growth and rising prices. Notably, ECB officials have warned that should oil prices breach the $150/bbl threshold, a recession in the Eurozone becomes a mechanical certainty. As central banks are forced to choose between fighting inflation or cutting rates to prevent a hard landing, gold remains the ultimate beneficiary of this policy dilemma, offering a liquid store of value in an increasingly fractured financial order.

Structural Central Bank Demand:

The ‘weaponisation’ of financial reserves following the Russia–Ukraine conflict has triggered a structural shift in central bank behaviour. A growing number of central banks are increasingly focused on diversifying their reserves, with gold emerging as a preferred asset. In periods of geopolitical stress, gold has reaffirmed its role as a liquid asset and a reliable store of value over the medium to long term.

Central banks are therefore expected to remain consistent buyers of gold, providing a strong structural pillar of demand. This trend is driven by continued reserve diversification and a gradual shift away from dollar-denominated assets. Even as the pace of purchases moderates from the peaks seen in 2023–2024, the baseline level of demand remains significantly higher than pre-2022 averages.

The broadening of the buyer base, with countries such as Malaysia and South Korea resuming gold accumulation in 2026, according to the World Gold Council, further reinforces this trend.

Unsustainable Global Debt Levels:

Global debt levels, now exceeding $300 trillion and trending higher toward record levels, are increasingly constraining central banks' ability to sustain elevated interest rates.

Dollar and Bonds:

Amid heightened geopolitical uncertainty, demand for the US dollar and US Treasury bonds has strengthened, reflecting a flight to safety. However, as tensions ease, this safe haven demand for dollar assets is expected to moderate, reducing upward pressure on the currency.

At the same time, elevated US real yields have acted as a key near-term headwind for gold. However, given rising global debt levels and signs of slowing economic growth, real yields are unlikely to remain sustainably high over the medium term. A moderation in both the US dollar and real yields is therefore expected to provide a supportive environment for gold prices.

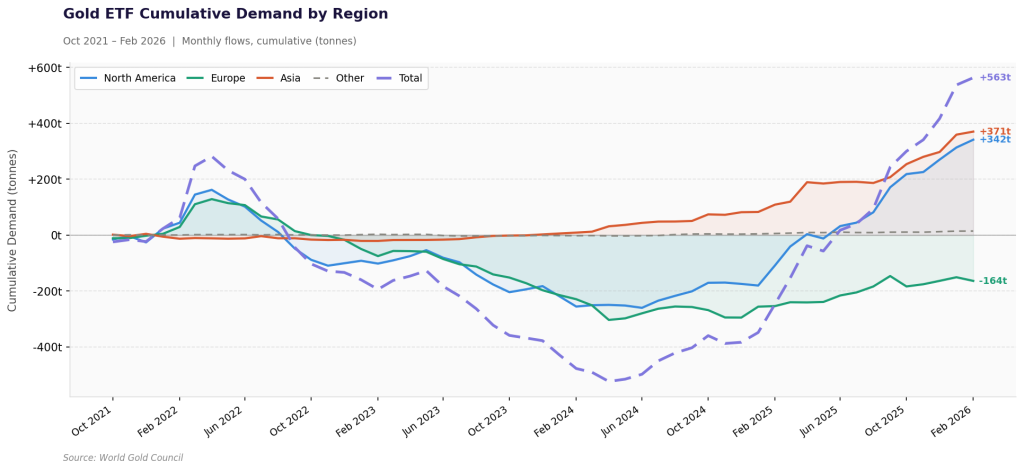

Financialisation of Gold (ETF Growth):

The growing adoption of gold ETFs, especially in key physical markets like India and China, is driving the financialisation of gold and expanding its investor base. This transition is enhancing liquidity and accessibility, while creating a more stable and scalable source of demand compared to traditional physical consumption.

Outlook:

Gold remains in a structural uptrend, though it is currently navigating a period of high volatility. After a sharp retracement from January’s record highs near 180000, it made a low of 129595 this month. After this, it is now seeing a relief rally and prices are currently consolidating near the 148500 zone.

In the near term, gold faces a formidable resistance at 155000. This level acts as a critical psychological and technical barrier. A sustained daily close above 155000 would signal the end of the corrective phase and potentially clear the path toward the 165000 to 170000 range. A retest of the previous all-time high near 180000 remains our target for 2026. Immediate support is near 144000 to 138000. Below that, 130000 is a strong support. The broader structure continues to favour a buy-on-dips strategy, with accumulation recommended during corrective phases.