In the ever-changing world of business analysis and investment, the asset turnover ratio stands out as a pivotal indicator of a company's operational efficiency. Investors, analysts, and lenders alike use this metric to understand how well a business is utilising its assets to generate revenue. For Indian companies and investors, asset turnover ratio offers essential insights when evaluating financial health, making strategic decisions, and benchmarking industry performance.

Understanding what asset turnover ratio is, how it’s calculated, and what it signifies can help you make more informed choices, whether you’re reviewing a listed company's annual report or considering a new investment. This ratio proves especially useful in the Indian economy, where sectoral differences mean that efficiency ratios can vary drastically across industries.

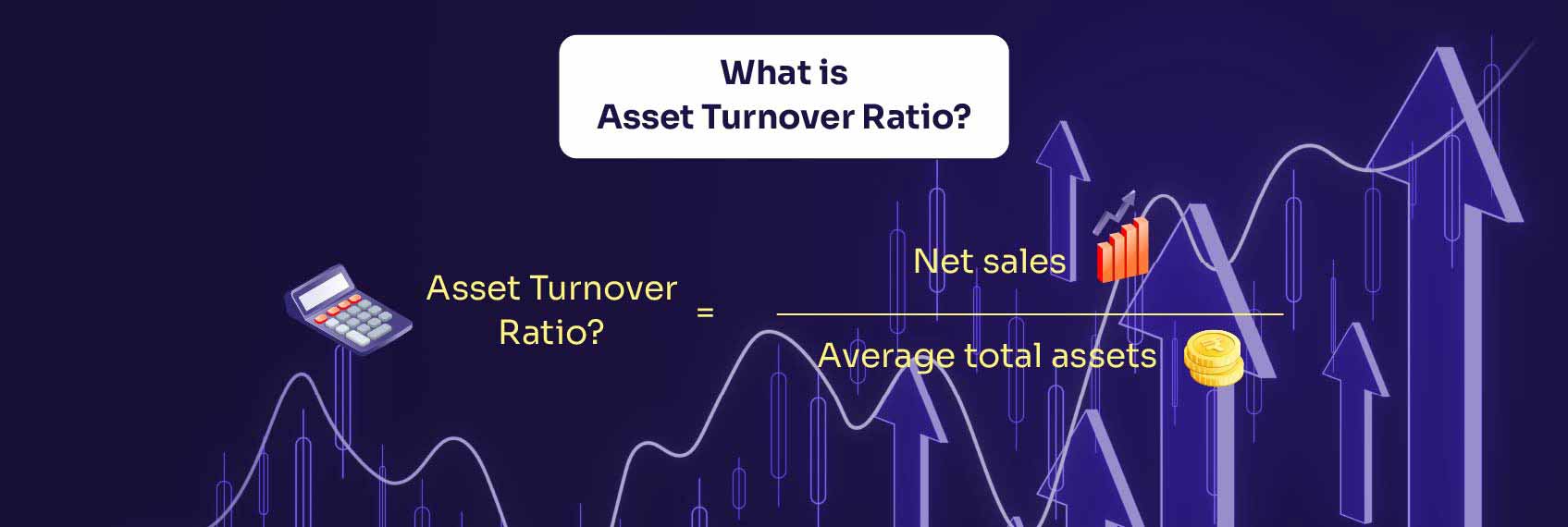

The asset turnover ratio is a financial metric that measures how efficiently a company uses its assets to produce sales. In essence, it answers the question: “How many rupees of sales does the business generate for every rupee invested in assets?”

A higher ratio usually indicates that a company is utilising its assets efficiently, while a lower ratio may signal under-utilisation or inefficiency. For better context, comparing the asset turnover ratio is most meaningful between companies that operate in the same industry.

Let’s break down the asset turnover ratio formula step-by-step:

Asset Turnover Ratio =Net SalesAverage Total Assets

Suppose Company A reports:

First, calculate average total assets:

Average Total Assets = ₹7,00,000 + ₹9,00,0002 = ₹8,00,000

Then, apply the formula:

Average Turnover Ratio = ₹50,00,000₹8,00,000 = 6.25

This means Company A generated ₹6.25 in sales for every ₹1 invested in assets during the period.

This ratio uses all asset classes, including both current and long-term (fixed) assets.

Total Asset Turnover Ratio = Net SalesAverage Total Assets

This variant uses net assets (total assets minus total liabilities), representing shareholders’ equity.

Net Asset Turnover Ratio = Net SalesNet Assets

Net assets can be found on the balance sheet as shareholders’ equity or calculated by subtracting total liabilities from total assets.

Comparisons are meaningful only within the same industry due to sectoral differences in asset structure and turnover cycles—e.g., a supermarket chain typically has a much higher ratio than a telecommunications operator.

Several internal and external factors influence this metric:

Some indicative benchmarks for Indian industries (based on published analyses and financial statements):

| Industry | Asset Turnover Ratio (Approx.) |

| Trading/Retail | 18.44 – 25.86 |

| FMCG | 2.09 – 3.07 |

| Infrastructure | 4.05 – 6.45 |

| Chemicals | 1.68 – 2.36 |

| Automobiles & Ancillaries | 2.00 – 2.37 |

| Telecom | 0.22 – 0.47 |

| Diamond & Jewellery | 9.39 – 12.37 |

Higher ratios (e.g., trading, retail) reflect rapid turnover and efficient asset utilisation, while lower ratios (e.g., telecom, infrastructure) result from high capital investments relative to sales.

The Asset Turnover Ratio is an important factor for evaluating operational efficiency in Indian businesses. By understanding the formula, its meaning, and the context-specific interpretation across industries, both investors and company directors are empowered to interpret companies’ performance, spot inefficiencies, and guide smarter investment decisions.

Before applying this ratio, always benchmark against industry peers and review trends over several years. For best practice, combine it with other financial ratios such as Return on Assets (ROA) and Net Profit Margin for a better assessment.

Gold: Tug-of-War Between Safe-Haven Demand and Macro Headwinds

3 min Read Mar 10, 2026

Bullion Demand Surges as Investors Rotate Back to Gold and Silver ETFs Amid Global Uncertainty

3 min Read Mar 10, 2026

NSE to Add Six Stocks to Futures & Options Segment from April 1, 2026

3 min Read Mar 10, 2026

Specialised Investment Funds (SIFs) in Indian AMCs

3 min Read Mar 10, 2026

Natural Gas: A Guide to India’s Trading Market

3 min Read Mar 9, 2026

For android only