Introduction

The Senior Citizen Savings Scheme was introduced by the Government in India in 2004. It is a relatively safe investment option offering stable returns, primarily for senior citizens above 60years of age. Individuals aged 55years and above who have retired on superannuation or super/ordinary voluntary retirement schemes, as well as defence personnel aged 50years and above, are also eligible to invest in this scheme.

SCSS Key Highlights

The top 5 must-knows of Senior Citizens Savings Scheme are captured below :

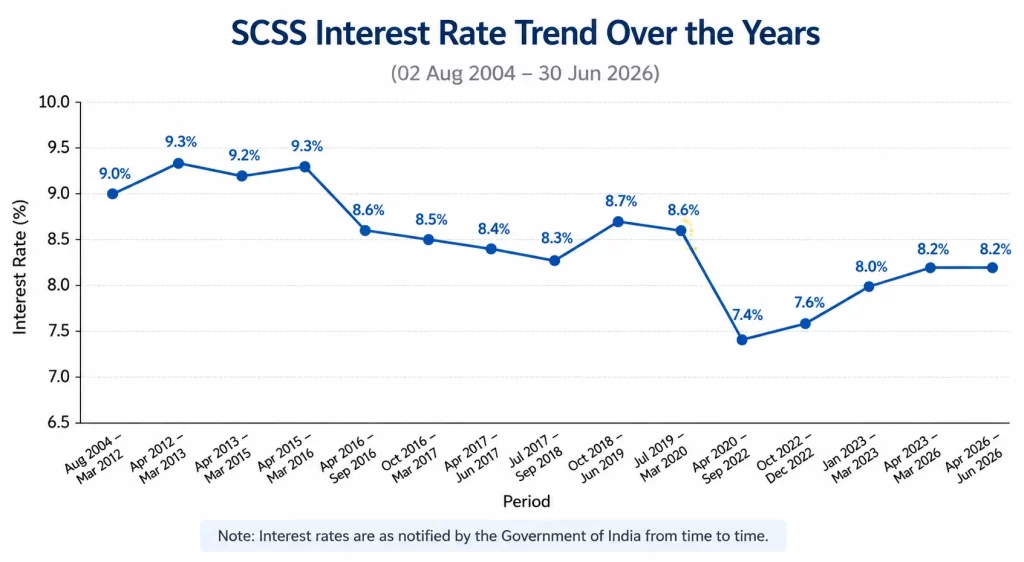

SCSS Interest Rate 2026

The current rate of interest applicable for SCSS for FY ‘26-27 is 8.2% per annum. While the government reviews and notifies the rate of interest every quarter (April, July, October, January), the key feature of SCSS is that once you lock in your investment, the rate of interest as on that date is fixed for the next 5 years.

This trend chart shows that after the decline between 2020-2022, the interest rate has recovered and fairly stabilised since January 2023, reinforcing the low volatility nature of this investment.

How SCSS Interest is Paid

- Interest is paid quarterly, i.e. April, July, October and January of every financial year

- The interest is credited directly to the bank account linked to the SCSS account.

SCSS Eligibility Criteria

Who can invest in SCSS ?

- Any Senior Citizen, i.e. Indian Citizens aged 60years and above

- Retired Individuals older than 55years, but lesser than 60years, who have retired on superannuation, Voluntary Retirement Schemes (V₹) or Super V₹ benefits.The SCSS account must be opened within 1 month of receiving your retirement benefits. Additionally, the SCSS investment account cannot exceed the total amount received from the retirement benefits

- Retired Defence personnel aged 50years and above. The SCSS account must be opened within 1 month of receiving the retirement benefits.

Who cannot invest in SCSS ?

- Non-Resident Indians (NRIs) or Persons of Indian Origin (PIOs)

- Member of Hindu Undivided Family (HUFs)

SCSS Benefits

There are multiple benefits offered by SCSS, which make it a very attractive investment option especially for retired persons :

Secure/Guaranteed Returns

Being backed by the Government of India, SCSS is a highly secure investment plan, with a guarantee of returns upto its maturity.

Attractive Interest Rates

SCSS is offering a good interest rate of 8.2% for 2026, which is higher than most other traditional options. At the time of investment, the rate of interest is locked in for the next 5 years (till maturity).

Quarterly Income Payouts

With a guaranteed rate of return at fixed intervals, SCSS investors can plan their cash-flows without any worry of market fluctuations.

Tax Savings

As a SCSS investor, you can claim tax deductions under Section 80C of the Income tax act (old tax regime), upto ₹1.5lakhs in a financial year.

Capital Protection

SCSS is shielded from stock market fluctuation and is hence considered relatively risk-free.

Tax Benefits of SCSS

It is important to understand the taxation implication linked to SCSS investments :

- The principal amount invested under SCSS is eligible for deduction under Section 80C of the Income Tax Act, under the old regime only. This deduction is available till a limit of ₹1.5lakhs.

- Interest earned from SCSS is completely taxable as per your respective income tax slab.

- If total income earned from SCSS exceeds the applicable threshold in a financial year, then TDS is applicable. Form 15G or 15H, as applicable, can be submitted to prevent TDS. Investors should verify the latest limits applicable to their income tax status, for the relevant financial year.

How to Invest in SCSS (Step-by-Step Guide)

Application process for SCSS is primarily offline and has to be done either through an India post office branch or an authorized bank branch. The only online facility currently available is that of downloading the form (either from India post or authorized bank website).

Step 1 - Verify your eligibility as a potential SCSS investor. You must be an Indian citizen 60years old or above OR a retired individual between 55-59years of age (if investing retirement benefits within 1 month of retirement OR a retired defence pe₹onnel aged 50 years or older

Step 2 - Keep your KYC documents ready, e.g. Aadhar, Pan card and 2 recent, passport size photos, alongwith age-proof. If you are retiring early, your proof of retirement and the retirement documents are required.

Step 3 - Visit an authorized bank or India Post office to obtain the SCSS application form. Alternatively, the form can be downloaded from the India Post or authorized bank website.

Step 4 - Fill up the SCSS application form with your required details, deposit amount and nominee information. Attach your self-attested KYC documents. The minimum deposit amount is ₹1000, while maximum is ₹30lakhs. For deposits under ₹1lakh, cash can be submitted while demand draft or cheque is required for amounts above ₹1lakh.

Step 5 - Once the application and documents are reviewed and verified, you will receive an SCSS passbook

Step 6 - Interest will be received quarterly to your linked savings account.

Deposit amount

SCSS vs Other Investment Options

The table below clearly shows how SCSS ranks as an investment option particularly for senior citizens/ retired pe₹ons :

| Feature | SCSS | Bank FD (Senior Citizen) | Post Office MIS | PPF |

| Current Return (2026) | 8.2% | 7.0–8.5%* | 7.4% | 7.1% |

| Risk Level | Very Low | Very Low | Very Low | Very Low |

| Government Backed? | ✅ Yes | ❌ No | ✅ Yes | ✅ Yes |

| Regular Income | ✅ Quarterly | ✅ Monthly / Quarterly | ✅ Monthly | ❌ No |

| Lock-in / Tenure | 5 years (+3-year extension) | 1–10 years | 5 years | 15 years |

| Maximum Investment | ₹30 lakh | No fixed limit | ₹9 lakh (Single) ₹15 lakh (Joint) | ₹1.5 lakh per year |

| Tax Benefits | Section 80C (subject to limits) | Only Tax-Saver FDs qualify | No tax benefit | Section 80C + tax-free maturity |

| Best For | Retirement income with high safety | Flexible capital protection | Predictable monthly cash flow | Long-term tax-efficient wealth creation |

*Rates vary depending on the bank, tenure and kind of senior citizen FD scheme.

Who Should Invest in SCSS?

SCSS as an investment option is ideal for :

- Retired individuals needing - Interest is credited on a quarterly basis, with the rate remaining fixed over a period of 5 years This helps them to plan their cashflow requirements.

- Risk-ave₹e investors - Stable returns are guaranteed by the government, not impacted by the volatile market forces

- Those looking for tax-saving + income - Twin advantages of tax benefit on investment account and fixed, quarterly income

Limitations of SCSS

There are 3 key limitations to investment in SCSS, which you should be aware of :

- Interest is fully taxable as per your respective income tax slab. Further, TDS is applicable if your total interest accrued exceeds ₹50,000 in a financial year.

- There is a lock-in period of 5 years, with premature withdrawal attracting a penalty (generally 1% to 1.5% of principal investment), depending on the holding period.

- Fixed interests restricts the ability of returns to be linked to inflation especially given the 5-year term.