Summary:

The global crude oil market has been thrust into extreme volatility following the onset of the Iran–US conflict on February 28, 2026. Prices spiked sharply during the initial phase of the war, with the Indian Basket briefly crossing $150 per barrel, before retracing on expectations of a ceasefire. Despite the current truce, set to run until April 21–22, the market remains structurally tight as supply disruptions and constrained shipping flows continue to distort global balances.

The global crude oil market has been thrust into extreme volatility following the onset of the Iran–US conflict on February 28, 2026. Prices spiked sharply during the initial phase of the war, with the Indian Basket briefly crossing $150 per barrel, before retracing on expectations of a ceasefire. Despite the current truce, set to run until April 21–22, the market remains structurally tight as supply disruptions and constrained shipping flows continue to distort global balances.

This report provides a concise overview of the crude oil lifecycle, along with a focused update on the evolving geopolitical landscape shaping current market dynamics.

Life Cycle of Crude Oil (From Extraction to Refined Products)

Crude oil is formed over millions of years from the remains of marine organisms buried under layers of sediment. Over time, heat and pressure transform this organic material into hydrocarbons. These hydrocarbons accumulate in underground reservoirs within porous rock formations, typically sealed by impermeable layers that prevent them from escaping. Such reservoirs are found both onshore and offshore.

Extraction: The Birth of a Barrel:

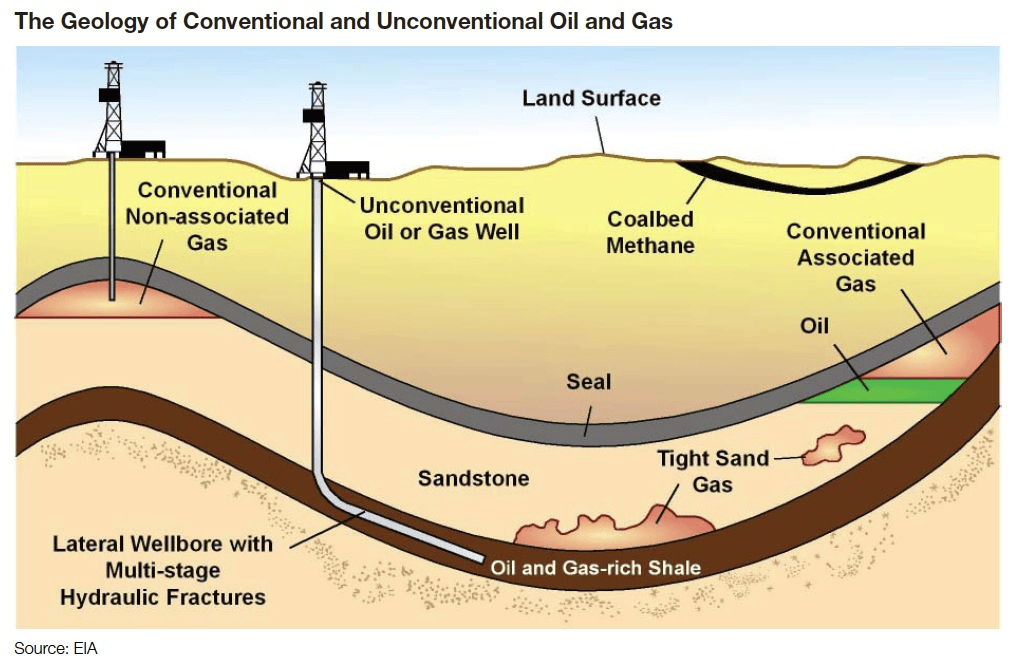

Crude oil is extracted by drilling wells into underground reservoirs. Broadly, extraction can be classified into two categories:

1. Conventional Oil Extraction: Conventional oil consists of liquid hydrocarbons that flow naturally or can be pumped using traditional wellbore methods. The oil resides in porous rock, much like water held within a sponge.

A large share of global conventional reserves is concentrated in the Middle East. Some of the largest conventional oil fields include the Ghawar Field (Saudi Arabia) and the Burgan Field (Kuwait).

Oil extraction occurs in three stages. Primary recovery (natural lift) uses reservoir pressure to bring oil to the surface, achieving ~5–15% recovery. As pressure declines, secondary recovery involves injecting water or gas to maintain pressure and push oil toward the wellbore, increasing recovery to ~20–30%. The remaining oil is extracted through tertiary (enhanced) recovery, using methods such as steam or gas injection (CO₂ or nitrogen) to reduce viscosity and improve flow. Total recovery can exceed 50% under favorable conditions.

2. Unconventional Oil Extraction: Unconventional oil refers to resources locked in low-permeability formations (like shale) that do not flow naturally. If conventional rock is a "sponge," unconventional rock is a "brick" the oil is there, but it is trapped.

It is extracted using two key techniques Horizontal Drilling and Hydraulic Fracturing (Fracking). In Horizontal Drilling the drill bit descends vertically and then turns 90 degrees, traveling laterally for miles through thin layers of shale to maximize reservoir exposure. In fracking, a high-pressure mixture of water, sand, and chemicals creates fractures in the rock. The sand keeps these fractures open, allowing oil to flow into the wellbore.

| Feature | Conventional | Unconventional (Shale) |

| Geology | Porous Rock (Sandstone/Limestone) | Impermeable Rock (Shale) |

| Well Profile | Vertical (mostly) | Horizontal + Fracking |

| Decline Rate | Slow (3–7% per year) | Rapid (60–80% in year one) |

| Cost Structure | High CAPEX: Billions to start a field. | High OPEX: Constant drilling needed. |

| Cycle Time | Long-Cycle: 5–10 years to first oil. | Short-Cycle: Months to first oil. |

| Price Elasticity | Inelastic (don't stop pumping if price drops). | Elastic (rigs stop moving as soon as price dips). |

Initial Processing:

At the production site, crude oil undergoes basic treatment to remove water, gases, and sediments. This stabilizes the crude and makes it suitable for safe storage and transportation.

Transportation:

Extracted crude oil is rarely consumed at its source. It must be transported to refineries, often across long distances and international markets. This makes transportation a critical component of the crude oil value chain.

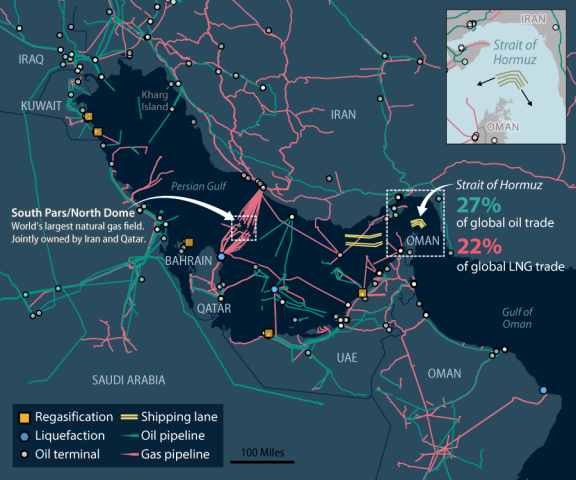

Crude is transported through multiple modes. Pipelines are the most efficient and cost-effective method for land transport, offering steady and large-volume flows. Their importance increases during geopolitical disruptions, as they can bypass key chokepoints such as the Strait of Hormuz. Currently, Saudi Arabia’s East West Pipeline, Iraq-Turkey Pipeline, and UAE’s Habshan-Fujairah pipeline are proving critical

For shorter distances or regions without pipeline infrastructure, trucks and rail are used, though at a higher cost.

For international trade, the dominant mode is oil tankers. These vessels vary by size and route:

| Vessel Type | Typical Route | Typical Cargo Capacity |

| Aframax | Short to medium haul | ~500,000 – 800,000 barrels |

| Suezmax | Can transit Suez Canal | ~1,000,000 barrels |

| VLCC (Very Large Crude Carrier) | Long-haul international trade | ~2,000,000 barrels |

| ULCC (Ultra Large Crude Carrier) | Largest capacity, limited routes/ports | ~3,000,000 – 4,000,000 barrels |

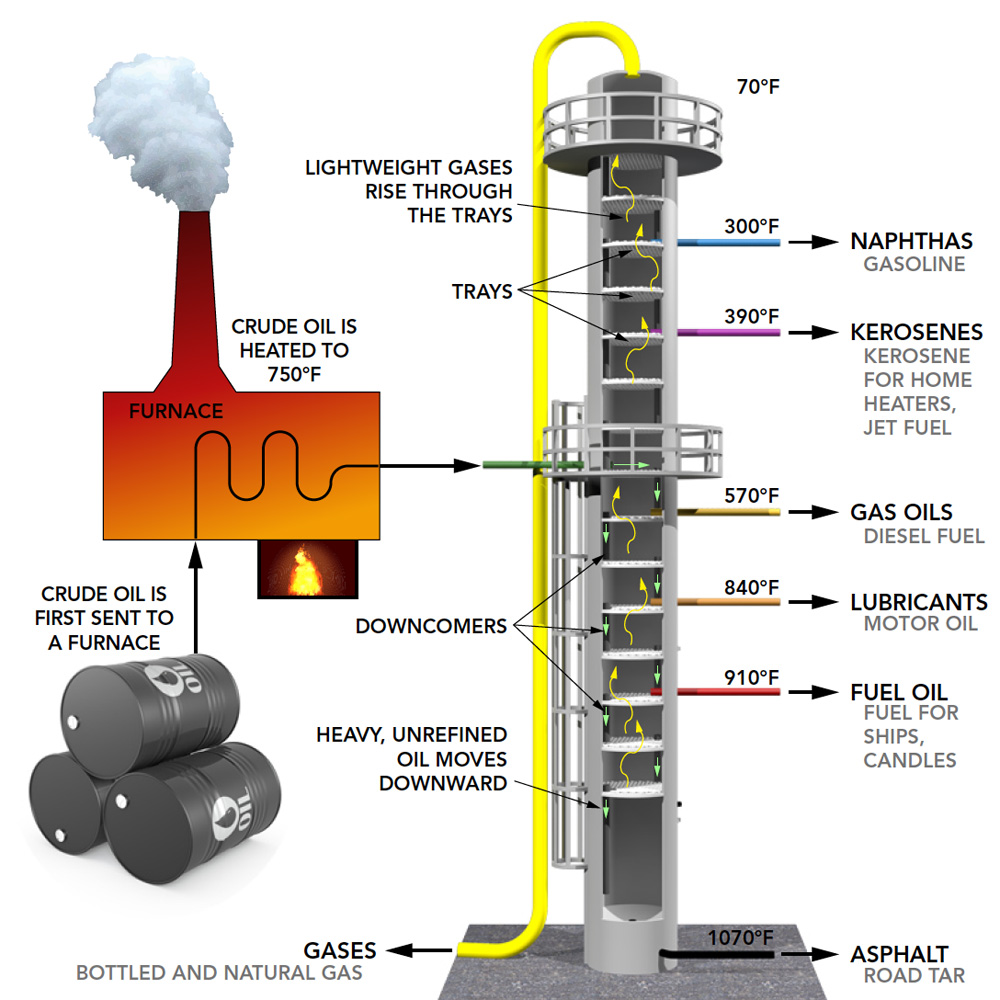

Refining:

Crude oil is a complex mixture of hydrocarbons and cannot be used directly; it must be separated into usable components. At the refinery, it is heated in furnaces and fed into a distillation column, where it is separated based on boiling points.

As the heated crude vaporizes and rises through the column, it cools. Different components condense at different heights, forming distinct layers called fractions.

Top (Light Fractions): LPG, naphtha, gasoline, petrol.

Middle (Distillates): Kerosene (jet fuel), diesel

Bottom (Heavy Fractions): Gas oils, fuel oil, bitumen

Lighter products rise higher in the column, while heavier products remain at lower levels. This initial separation forms the basis of refining, after which further processes are used to increase the yield of high-value fuels.

To make a heavy barrel profitable, refineries must upgrade the heavier fractions at the bottom of the distillation column into lighter, higher-value fuels. This process, known as conversion, is primarily carried out through cracking, where heat, pressure, catalysts, and sometimes hydrogen are used to break large hydrocarbon molecules into smaller ones. Cracking units are complex systems consisting of reactors, furnaces, and heat exchangers. Advanced refineries operate multiple types of units, including fluid catalytic crackers (FCC) and hydrocrackers, allowing them to maximize the yield of valuable products such as petrol and diesel.

Following conversion, the products undergo desulfurization (sweetening). Most crude oil contains sulfur, which causes pollution and corrosion. Through hydrodesulfurization, sulfur is removed to produce cleaner fuels that meet environmental standards.

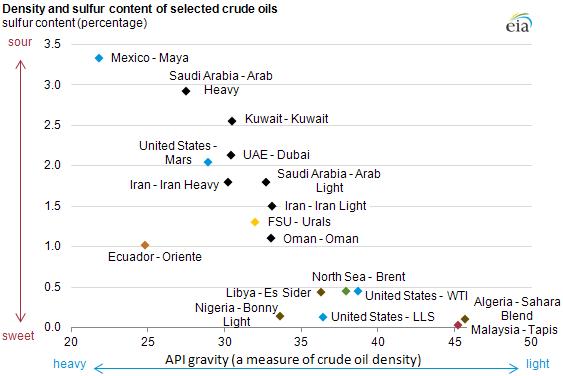

This creates the sweet vs sour crude dynamic. Sour crude trades at a discount due to higher sulfur content and additional processing requirements, while sweet crude commands a premium.

Both crude oil and refined products are stored temporarily in large tank farms near the refinery. From there, pipelines, rail, and trucks transport the final products to distribution networks and end users.

If we can sweeten all oil, why don't we?

Even the heaviest, most sulfur-rich crude can be converted into lighter fuels, but the constraint is cost, not chemistry. Upgrading and desulfurization require large amounts of hydrogen, typically derived from natural gas. When natural gas prices are high, processing heavy or sour crude can become uneconomical.

Refineries differ in capability. Simple refineries can process only light, sweet crude, while complex refineries use advanced units such as hydrocrackers and cokers to handle heavy and sour grades and maximize high-value output.

It is neither practical nor desirable to convert all crude into light fuels. Heavier fractions remain essential, with bitumen used in roads and roofing, and bunker fuel used in marine transport.

| Crude Name | Origin | Type | Sulfur Level | Physical State | Trader’s Note |

| WTI | USA | Light | Sweet | Water-like (Thin) | The US benchmark. Extremely high gasoline yield. Very easy to flow through pipes. |

| Brent | North Sea | Light | Sweet | Light Syrup | The global price floor. Slightly "heavier" than WTI but still very high quality. |

| Arab Light | Saudi Arabia | Medium | Sour | Olive Oil | India's Staple. The "workhorse" for Indian refineries. High reliability and consistent volume. |

| Basra Medium | Iraq | Medium | Sour | Motor Oil | Top India Import. Iraq is often India's #1 supplier. It’s "grittier" than Arab Light but cheaper. |

| Urals | Russia | Medium | Sour | Heavy Oil | The 2024-26 Surge. Since 2022, this has become a massive part of India’s diet due to steep discounts. |

| Murban | UAE | Light | Sweet | Thin Juice | Highly prized for its high yield of middle distillates like Jet Fuel and Diesel. |

| Maya | Mexico | Heavy | Very Sour | Cold Molasses | Very thick. Only "Complex" refineries (like Reliance Jamnagar) can handle this profitably. |

| WCS | Canada | Heavy | Very Sour | Tar / Bitumen | The thickest on the market. Usually must be diluted with chemicals just to get it to flow through a pipe. |

| Sahara Blend | Algeria | Ultra-Light | Sweet | Acetone-like | Almost transparent. So light it’s often called a "condensate." Used to boost gasoline octanes. |

Current Scenario:

Seven weeks into the Iran–US conflict, the situation has shifted from active warfare to a fragile diplomatic stalemate. Following failed direct talks in Islamabad, a temporary ceasefire remains in place until April 21–22, with ongoing efforts by intermediaries such as Pakistan, China, Turkey, and Russia to extend it. Bloomberg reports indicate both sides are exploring a short-term extension to avoid further escalation.

The Strait of Hormuz has moved from a hard blockade to a conditional reopening. While Iranian Foreign Minister Abbas Araghchi has declared the passage open during the ceasefire, actual tanker flows remain constrained due to security risks and elevated insurance costs. The U.S. Department of Defense continues to monitor stalled vessels, highlighting lingering disruption.

Before the conflict, Hormuz handled around 15 mbpd of crude and product exports, with India and China as key buyers. Since then, over 60 energy facilities have been impacted, and approximately 11 mbpd of production has been taken offline. Export flows have fallen to ~7 mbpd, while refinery run cuts have reduced demand by an additional ~3 mbpd.

Despite the scale of attacks, the disruption has been driven primarily by logistical constraints rather than permanent infrastructure damage, with restricted shipping through Hormuz acting as the main bottleneck.To offset disruptions, Saudi Arabia and the UAE have maximized alternative routes. The East–West Pipeline and Habshan–Fujairah (ADCOP) pipeline are operating near full capacity, together redirecting a significant portion of exports. However, these routes offset only ~40% of normal Hormuz flows, keeping the global market tight.

Looking ahead, the next round of US–Iran talks and the April 21–22 ceasefire deadline remain key triggers. While the reopening of Hormuz has eased some risk premiums, uncertainty remains elevated. If hostilities resume, there is a significant risk of renewed Hormuz closure, along with potential escalation by Houthi forces targeting the Bab el-Mandeb Strait, further disrupting global oil flows.