In financial markets, long-term investment outcomes are often determined by identifying how an investor structures their overall portfolio. This structure is commonly referred to as asset allocation. It plays an important role in managing market volatility, keeping up with inflation and the evolving financial goals across different life stages.

For Indian investors who typically have access to equities, fixed-income instruments, gold, real estate, and cash equivalents, asset allocation planning offers a framework for diversification without relying on forecasts or speculative judgement.

What is asset allocation?

Asset allocation refers to the distribution of an investment corpus or capital across multiple asset classes, with the objective of diversification. This helps to reduce risk and protects your capital in the long-term as it grows. It involves deciding how much exposure a portfolio should have to broad categories such as equities, debt, gold, real estate, and cash equivalents rather than focusing on one category.

| Asset class | Examples of allocations |

| Equity | Listed shares, equity mutual funds, index funds, ETFs |

| Debt or fixed income | Bonds, debt mutual funds, PPF, EPF, NPS, bank deposits |

| Gold | Physical gold, Gold ETFs, Sovereign Gold Bonds |

| Real estate | Residential or commercial property, REITs |

| Cash and equivalents | Savings accounts, overnight or liquid funds |

This overall allocation provides the structure within which individual products and securities are selected.

Why asset allocation matters

Every asset class often has a different reaction, based on different economic conditions. For example, Indian equities may show sharp short-term fluctuations, while high-quality debt instruments may show more stable price movements. Gold may behave differently during periods of currency weakness and global uncertainty.

By combining multiple asset classes within a portfolio, investors may reduce the impact of poor performance in any single category.

Key reasons asset allocation plays a critical role include:

Risk distribution: Exposure is spread across assets rather than concentrated in one category such as equities or fixed deposits.

Goal alignment: Long-term goals such as retirement usually need a growth-orientated asset, while short-term goals may prioritise stability.

Behavioural discipline: A predefined asset mix can help investors avoid emotional decisions during market cycles.

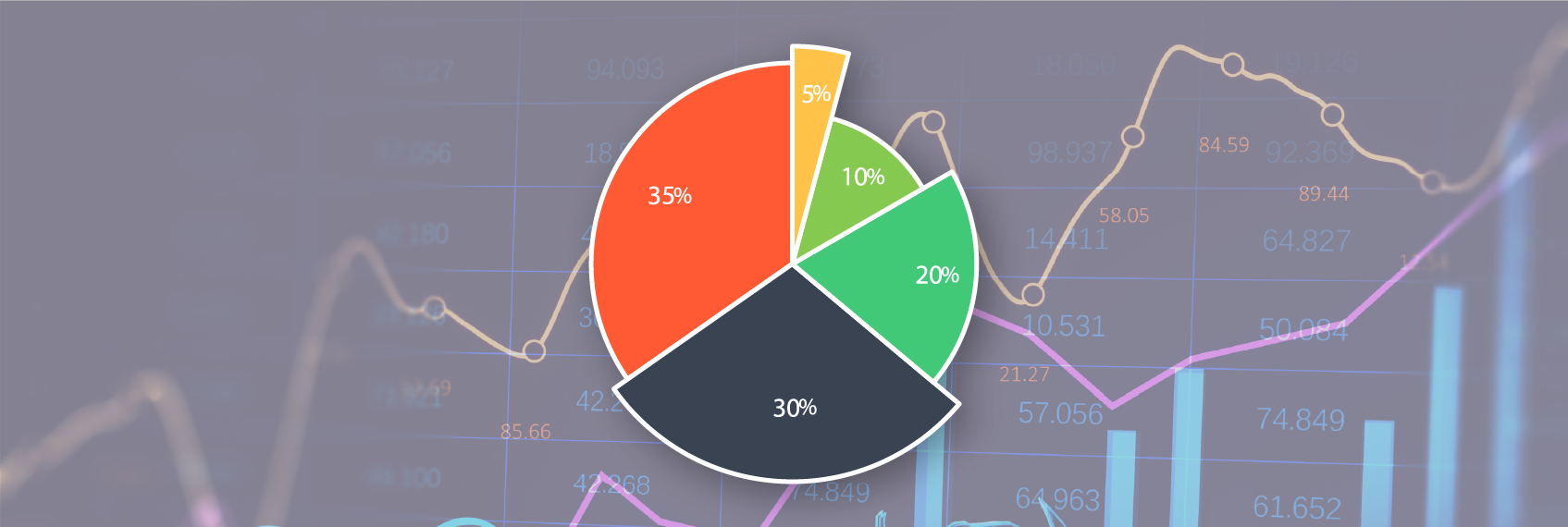

A helpful way to visualise asset allocation is as a pie chart, with each slice representing an asset class in proportion to its role in the portfolio.

Age-based asset allocation

Many investors are taught about asset allocation through the concept of age-based allocation. A commonly quoted rule is the “100 minus age” rule traditionally used to approximate equity exposure. Though overly simplistic, such rules illustrate how an age and time horizon can influence the allocation structure.

For instance, an investor aged 25 to 30 might be inclined to invest heavily in equity and less in debt and other assets, whereas an investor aged 35 to 45 might take a moderate to high equity position and quite high exposure to debt.

Individuals aged 50 to 60 might cut down exposure to equity, whereas individuals aged 60 and above will tend to have a low equity exposure and higher allocation to debt and other less volatile instruments such as FDs.

Age being just one factor, other equally important factors would be the stability of income, liabilities, liquidity requirement and risk appetite with volatility.

Thinking about asset allocation and risk appetite

There is no right or wrong when it comes to asset allocation. SEBI also has regulations that restrict advice about asset allocations without a detailed analysis. Rather, it is best to think of asset allocation structures as general guidelines that combine both risk tolerance and time horizon.

For example, a short-term investor with lower risk comfort may prefer a higher preference towards debt and cash.

Conversely, a long-term investor with higher risk comfort may lean towards equities with diversification.

In practice, investors may use a mix of direct equities, mutual funds, fixed income instruments, gold, real estate, or hybrid products. It is important to review your portfolio regularly and adjust your asset allocations considering all factors.

Conclusion

Every investor must focus on asset allocation as a principle to help build a diversified portfolio. They should create a portfolio with a mix of asset classes such as equity, debt, gold, real estate, and cash. Also, one must remember that no single allocation type suits everyone, and it is based on factors such as age, risk appetite, and time horizon.