All is fair in love and war—William Shakespeare

Fair! But what if love is a one-way street?

One–sided love stories often become war stories.

One such story is unfolding on India’s corporate canvas.

As you may know, L&T, one of India’s largest and oldest construction companies, is seeking to acquire Mindtree, a gen-Z mid-sized Information Technology (IT) company.

The present management of Mindtree isn’t keen on relinquishing control of the Company and is calling it a hostile takeover. However, L&T is still in persuasion mode.

SN Subrahmanyan, CEO of L&T has gone on record saying, There are certain emotions and trepidation involved, but business is business. Emotions do play a part, but emotionalities have to be overcome as we go forward. What we are trying to do, is with, if I can use the word ‘pyaar’, and we will continue to look at it as something we are doing from our ‘dil’. And we will continue to look at it in the same manner and purpose.

Oh dear! Such high-voltage melodrama befits Bollywood not the boring and mundane corporate universe, right?

Is it really love or only business?

The devil is in the details.

VG Siddhartha, the founder of Coffee Day Enterprises, is selling his company’s stake as well as his personal stake (20.4%) in Mindtree to L&T for an approximate consideration of Rs 3,400 crore.

This deal would make L&T the single-largest shareholder. But L&T’s ambitions are much bolder. While launching an open offer for existing shareholders, it hopes to take its shareholding to 67% by acquiring enough shares too from the open market.

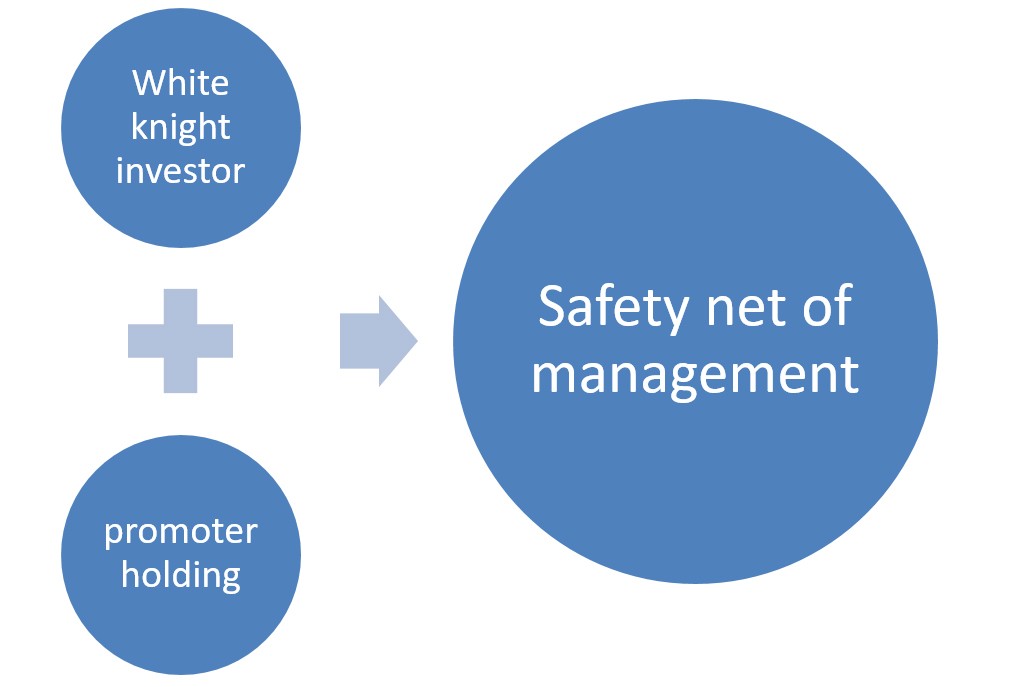

Unfortunately, promoters/founders hold only a 13.3% stake in the Company. Such a low promoter holding doesn’t bode well for the existing management. If L&T succeeds in taking control of the Company, it’s likely to merge it with L&T Infotech.

Many of you might wonder how the shareholding of a non-founder shareholder (VG Siddhartha) went as high as 20.4%. Well, equity dilution happens for various reasons, including the expansion of the business or even the monetisation of it.

Going by the account of Ashok Soota, a co-founder of Mindtree who has already exited the Company, VG Siddhartha, along with his Coffee Day Enterprises, has been a white knight for the company for past 9 years.

Note: In plain English, a white knight investor is a stakeholder that is sympathetic to the existing management and shields the company from hostile takeovers.

Now that the black knight, L&T, is replacing VG Siddhartha, the only possible option left with the present management is to find another white knight to counter L&T’s potential takeover attempt. In essence, drawing a long term plan to combat L&T is an arduous task.

The L&T group has founded two IT companies already —L&T Infotech and L&T Technology Services.

What might then be driving L&T to shell out close to Rs 10,800 crore to add one more IT company to its pack?

(Source: ACE Equity, company annual report)

You see, L&T Infotech and Mindtree have complementary business profiles. If the same management controls Mindtree and L&T Infotech both, tapping growth opportunities might become more comfortable for the consolidated entity. It’s clear L&T is eying synergies between L&T Infotech and Mindtree. To be specific, it might also be looking at Mindtree’s digital revenues.

As per media reports, there isn’t much overlap in the clientele of both the companies. This makes two mid-sized IT companies compatible. Thus, L&T’s stand of allowing Mindtree to continue as a separate entity might be temporary, perhaps, until it strikes a deal with the present management.

(Source: Company Annual Report)

Retail, Consumer Packaged Goods (CPG), Manufacturing (RCM)

Banking, Financial Services and Insurance (BFSI)

Technology, Media and Services (TMS)

Travel and Hospitality (TH)

(Source: Company annual report)

(Source: Company annual report)

(Source: ACE Equity, company annual report)

A typical Mindtree employee enjoys working with friendly management, in an environment wherein there isn’t any strict dress code, the hierarchy is lenient, and the work environment is flexible.

As against that, L&T’s work culture is more traditional and less flexible.

Will that result in higher attrition?

That would be a challenge for L&T. Will they change with the time and prove critics wrong?

It’s anybody’s guess at the moment.

The cultural transition isn’t smooth, many a time. And organisational culture flows from top to bottom.

Let’s not forget, human capital is the most valuable asset of any IT company. If, the present management manages to move its people and clients out of Mindtree (to some new entity they might form in future or elsewhere), buying Mindtree would be nothing less than buying a white elephant for L&T. But it’s easier said than done!

Global experts on mergers and acquisitions believe hostile takeovers are seldom successful and they rarely result in a win-win situation. Therefore, the real test of L&T would be to take the present management along and pacify it with the appropriate role/compensation or any suitable arrangement.

For now, builders have arrived with chainsaws and bulldozers. It might be too late for Mindtree founders to start the Chipko movement against bullying builders.

Foreign Portfolio Investors (FPIs) and mutual funds collectively hold close to a 49% stake in the Company. And they are unlikely to part ways with their equity unless L&T sweetens the deal for them. Many of them opined that Rs 980, the price L&T paid to VG Siddhartha, is unattractive.

Given that, the present management has little or no options left. Accordingly, steadying their nerves and waiting for L&T’s next move might be a sensible move for investors, rather than selling in distress.

Why should you be subject to pyaar ke side-effects?

You as an investor should appose all proposals and choose the best one for you…

Kyon ki bhaiya sabse bada rupaiya!

For android only

Post your comment

You must be logged in to post a comment.